IN A WORLD OF BIG DATA, services have access to a frustrating quantity of information about customers. From demographic information to a financial obligation to costs routines, virtually all elements of our monetary life is tracked.

“Essentially, whatever is understood about us,” says Beau Henderson, CEO of financial company RichLife Advisors in Atlanta. The obstacle for business is identifying how to condense all that info to make it quickly available and functional. To do that, various customer reports and scores have been developed.

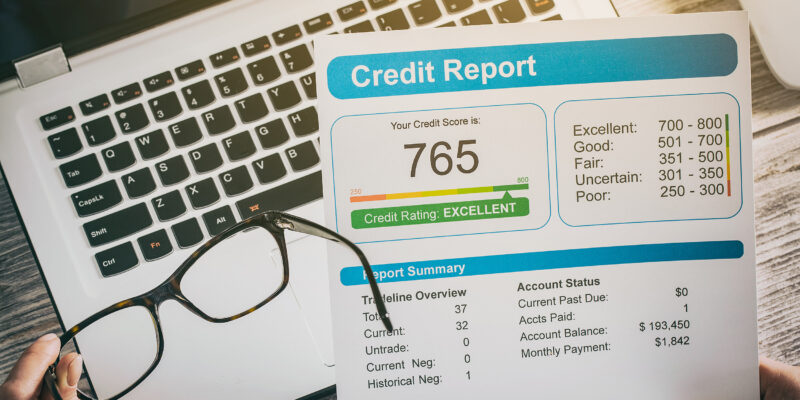

While credit reports are the most typically known data point, it hasn’t constantly been that way. “Three years ago, we didn’t even understand about those,” Henderson says. Nevertheless, with credit reports being utilized commonly in loan application choices and interest rate calculations, they have become far more noticeable and understood in current years. Now, the customer scoring market has expanded and a new age of under-the-radar reports provide details on a person’s home loan claims, insurability, and more.

Continue reading to discover little-known customer reports and ratings that might impact your monetary health and how businesses market their services and products to you.

Specialized credit rating. Credit scores are provided to customers free of charge by numerous charge card businesses, banks and websites, but those 3 digits might not be the very same as the ones used by banks. “A lender may see a rating that’s a little bit various than that,” states Theresa Williams-Barrett, vice president of customer loans and loan administration for Affinity Federal Cooperative Credit Union in New Jersey.

The credit history firm FICO offers at least 29 different credit histories, including some that are specifically developed for industries such as home loans and bank cards. Additional ratings are offered from the business VantageScore.

Williams-Barrett states the distinction between the credit report provided to consumers for totally free and those bought by loan providers can be significant. A rating developed for mortgage loan providers for insights may weigh debt usage and other factors differently in order to better estimate whether somebody will be able to maintain payments.

AnMIB Customer File. If you have requested an individual life, health, or similar insurance coverage within the past seven years, you’ll have a MIB Consumer File. Maintained by the MIB Group, a subscription company for the insurer, this record consists of details such as whether a previous policy application has been rejected and for what reason. Insurance coverage companies utilize it to identify misinformation or omissions when evaluating a current application. Consumers are entitled to request one totally free copy of their consumer file each year from the MIB Group. The report can be requested either online or by phone.

An Insurability Rating from the contrast site The Zebra. Unlike other ratings on this list, the Insurability Score was developed to assist customers, not insurance companies. Established by the vehicle insurance coverage contrast site The Zebra, the rating rates users on a scale of 950 using data they supply. In addition to calculating ball games, the business supplies suggestions for enhancing the potential customers of being authorized for protection at a lower rate. Such tips may include maintaining constant protection and enhancing credit history.

“Our name is The Zebra due to the fact that our company believes in attempting to make insurance black and white,” says Joshua Dziabiak, co-founder of the site. Details provided by customers in order to receive an Insurability Rating is just shared with insurance companies for the purposes of getting quotes. “We’re not in the organization of generating income from data,” Dziabiak states.

ASmartLinx individual report. Offered by the business LexisNexis, this report gathers data from 13,000 proprietary and public sources to determine how individuals are connected. It includes an individual summary, consisting of a physical description, together with licensing info, organization connections, arrest history, and other data. The company touts the report as a method for companies to prevent fraud, regulative threats, and money laundering. Customers can ask for a copy of the information LexisNexis utilizes to develop its individual reports.

CLUE reports.LexisNexis also provides insurers several Comprehensive Loss Underwriting Exchange, or CLUE, reports. “This is basically a claims report,” Dziabiak says. With variations readily available for car, home, and industrial coverage, these reports let insurance companies see what claims have been made and just how much has been paid out within the past 7 years.

“The majority of the major insurer contribute to it,” Dziabiak notes. LexisNexis will supply customers with a free copy of their reports every 12 months. Consumers can ask for a copy online or through the mail. Your name, birth date, and Social Security number are needed to obtain a report.

A-PLUS Residential or commercial property report. The A-PLUS Property report serves the same purpose as the IDEA report. Used by the data analytics firm Verisk, the report offers claims data and can evaluate it to flag specific losses. The business can likewise assist insurance companies to determine whether a specific candidate has a claims history that necessitates more evaluation. Verisk supplies consumers with one complimentary A-PLUS Home report every 12 months.

A ConsumerView success rating. A product from the credit reporting bureau Experian, the ConsumerView Success Rating is meant for those sending “invitation-to-apply” marketing products, such as charge card deals. It recognizes families more than likely to pay their financial obligations and ranks them on criteria like their expected success and possibility of reacting to an offer and being accepted.

Discretionary Costs Index. The Discretionary Spending Index is another item designed for online marketers. Created by the customer credit reporting firm Equifax, the index scores homes on a 1,000-point scale using a combination of known customer information, such as earnings and financial investment properties, along with other signs to figure out discretionary costs potential. The ranking isn’t indicated to be utilized for lending decisions, however rather determines customers who may be receptive to upselling or cross-selling.

DonorScores from the research study and analytics business DonorTrends.Even your potential to contribute to an excellent cause is ranked and scored in today’s world. DonorTrends, an independent research company, uses analytics to create ratings and assist fundraisers to determine which people are more than likely to donate and then give more. Ball games depend on data already understood by a charitable organization and don’t pull information from third-party sources.

Comments